Perpetrators

This is a list of the people that bear responsibility, for the creation and support of the Bindingsteuer and who promised to kill it but do not deliver.

Note: The photographs are from the public profiles on Bundestag website and the Bayerischer Landtag .

SPD - Olaf Scholz

Bundestag Profile | abgeordnetenwatch.de Profile | Wikipedia (de) | Wikipedia (en)

Chancellor today and Finance Minister when the Bindingsteuer was enacted and ignoring the advice coming from the Bundesrat to stop it. He has never made any statement, but he bore maximum responsibility as the Minister in charge.

Speculated to be the "other ministries" veto issuer to stop the death of the Bindingsteuer in the Future Financing Act (Zukunftsfinanzierungsgesetzt). See FDP - Florian Toncar - Veto from Other Ministries

SPD - Lothar Binding

Bundestag Profile | abgeordnetenwatch.de Profile | Wikipedia (de) | Wikipedia (en)

The, allegedly, intellectual author. SPD Finance Speaker and member of the Finance Committee in Parliament. Retired.

Given the length of the content, there is a full-blown section.

For details see: Lothar Binding - The Long Play Edition ....

SPD - Michael Schrodi

Bundestag Profile abgeordnetenwatch.de Profile | Wikipedia (de) | Wikipedia (en)

Binding's successor as SPD Finance Speaker, member of the Finance Committee in Parliament and vocal supporter of the Bindingsteuer with the same "mock the trader" arguments.

Here is the last question about the Bindingsteuer he answered with regards to the Bindingsteuer on Jul 18th, 2023 and which is also part of the The Undoing ...

Summary: "Expropriation" is well aligned with the interests of the general public.

Link: abgeordnetenwatch.de - Michael Schrodi 2023-07-18

Question (translated)

Loss Offsetting for Futures Transactions: Do the legal effects align so completely with the goals of the SPD that you see no need for changes?

Three reasons are cited for the limited loss offsetting for futures transactions:

1. Closing tax loopholes

2. Preventive deterrence

3. Avoidance of unilateral sharing of lossesHowever, it is not just about closing a tax loophole. The majority of those affected are likely to be tax-compliant private investors.

Deterrence does not primarily work preventively. Many private investors are unaware of the legal regulations. Only upon receiving tax assessments (and thus too late), are private investors deterred.

It is not only the unilateral but any sharing of loss transactions above €20K per year that has been excluded. The result is a unilateral sharing of profits.

I have incurred a significant loss. In addition, I am supposed to pay a similar amount in taxes. I perceive this as a punishment. Small government parties and the CDU see the need for changes. Only my party of heart does not...

Answer (translated)

With the current regulation, losses from futures transactions can only be offset against profits from futures transactions and income from option premium transactions. Loss offsetting is limited to €20,000. Uncompensated losses can be carried forward to subsequent years and offset in each year up to €20,000 against profits from futures transactions or option premiums. The limitation on loss offsetting in futures transactions is justified, as these transactions typically involve risky financial bets without a real economic hedging purpose. In our view, speculative purposes should not fully burden the general public in case of losses.

The restrictions do not deny loss offsetting but rather extend it over time. Small investors generally receive immediate tax consideration for their losses. For investors with higher assets, the limitation on loss offsetting is justified, as they benefit from the low flat tax rate of 25 percent on their more substantial capital gains. At present, the SPD parliamentary group sees no reason to change the existing regulation.

We consider the current regulation to be in line with the constitution and well-aligned with the interests of the general public.

Wow!

Let' quickly analyze the answer:

The Key Wrong Points

-

Expropriation is well-aligned with the interests of the general public. A classic in banana republics.

-

"risky financial bets", because who would use them to protect a portoflio as pointed out by the Bundesrat - Report

-

He has no problem in making false statements, like "speculative purposes, should not fully burden the general public in case of losses"

-

And hey, of course, he mentions that losses are not lost, but can be carried over to the following years. As if they were recoverable:

- Ask Real Case - Max ...

- ask the Bundesrat - Report ..., in which the non-recoverability and eternal growing is already stated.

SPD - Dirk Wiese

Bundestag Profile | abgeordnetenwatch.de Profile | Wikipedia (de) | Wikipedia (en)

Herr Wiese himself was not on the Finance Committee that brought the Bindingsteuer to you. He is an example of party discipline, having voted for something not fully understood.

Having been asked about the impact of the Bindingsteuer with a question specific to "Taxes on Losses", the answer shows a complete lack of understanding, repeating the same fake mantra that losses are financed by other taxpayers.

And he believes the expropriating nature of the law to be constitutional.

But the answer goes beyond that because he then says:

Such losses can be offset against profits from such financial bets during the year

Et voila! That this offsetting is limited seems to be ignored. People can simply offset.

He then goes on to say:

Losses that cannot be offset in the year of their occurrence can be offset against profits of the following year up to 20,000 euros. Loss offsetting is therefore possible, but it is stretched over time

Which losses? Because the previous statement said they can be compensated. Furthermore, the statement also forgets that carrying over is also limited and fake.

He obviously asked around, most probably Herr Roth, whom he quotes and shows that his understanding of the Bindingsteuer is a pure hearsay thing. Pen, paper and 5 minutes of basic match would have helped.

Taxes on Losses are constitutional

Question (translated)

Do you personally consider taxes on losses to be constitutional?

In your recent response regarding § 20 Abs. 6 Satz 5 EStG, you mentioned that one must await the courts' opinion on its unconstitutionality. But does this apply even when the legal situation is entirely clear?

A brief CFD example:

Profits: 60,000 euros

Losses: 65,000 euros

Tax: 10,000 eurosI find it impossible for the Federal Constitutional Court (BVerfG) to "approve" such a thing. The law is already unlawfully established; otherwise, it would not have worked. I don't know if you are aware of the background. Please inquire with Lothar Binding.

Please form your own opinion on this and especially whether this law is worthy of a constitutional state.

Answer (translated)

As my colleague Michael Roth from our parliamentary group has already responded to your identical question, we consider the current regulation to be constitutional.

I would like to quote his response: "In the draft bill for the Future Financing Act, the elimination of loss offsetting circles for losses from futures transactions and losses on private claims was initially planned. These provisions were removed in the departmental coordination. The Bundestag passed the amended draft law for the Future Financing Act on November 17, 2023.

This concerns a restriction on the losses of private individuals from speculative futures trading. The loss offset restriction does not apply to losses of companies. As the SPD parliamentary group, we advocate the position that such losses from risky financial bets should not be financed unlimitedly by the taxpayer. Such losses can be offset against profits from such financial bets during the year. Losses that cannot be offset in the year of their occurrence can be offset against profits of the following year up to 20,000 euros. Loss offsetting is therefore possible, but it is stretched over time. We consider this regulation to be constitutional.

CDU/CSU - Ralph Brinkhaus

Bundestag Profile | abgeordnetenwatch.de Profile | Wikipedia (de) | Wikipedia (en)

Even if the SPD was in charge of the Ministry of Finance and Binding happened to be the intellectual author and pusher, the CDU/CSU was a needed cooperator. And Ralph Brinkhaus was the parliamentary leader of the group.

It is not that the CDU/CSU was a passive perpetrator, it was an active one, as recorded when the Bindingsteuer amendment was introduced. The CDU/CSU simply recorded that it had been "difficult" for the party to reach a compromise with the SPD. See The Finance Committee Smoking Gun

Herr Brinkhaus, being a Tax Advisor himself, should have known better.

As Parliamentary Group Leader he holds maximum responsibility for the birth of the Bindingsteuer for having achieved a political arrangement with the SPD. Apparently in exchange for thingies for the electro-mobility mode.

The "compromise" was additionally confirmed by another party member. See below.

CSU - Petra Guttenberger

Bayerischer Landtag Profile | abgeordnetenwatch.de Profile | Wikipedia (de) | Wikipedia (en): N/A

Frau Guttenberger as most, including Herr Brinkhaus, did not and do still not understand that expropriation was legalized with the Bindingsteuer.

See, someone asked Frau Guttenberger and the one-line summary of her answer is

Political Compromise

Ultimately, the regulation was supported in a political compromise to prevent more extensive limitations.

Wow! Implementing the law which gives direct and unlimited access to the pocket of taxpayers was a simple political compromise.

Can they even count to 100 without using their fingers? Because it is obvious that basic math escapes the skills of many Members of Parliament. It would be worse if it had to be assumed they knew what they were doing and what the consequences were: expropriation.

Question and Answer to Petra Guttenberger

Question (translated)

Why has the Bavarian State Government not initiated a procedure for abstract norm control against § 20 Abs. 6 Satz 5 EStG so far? Dear Mrs. Guttenberger,

At the end of 2019, the restriction on loss calculation in § 20 Abs. 6 Satz 5 EStG for futures transactions was enacted. It is undeniable that this regulation violates Art. 3 Abs 1 GG, leading to taxes on losses or tax rates > 100%.

Example:

Profits: 100,000 euros

Losses: 120,000 euros

Tax: 20,000 eurosOn October 9, 2020, the Bavarian Broadcasting Corporation (BR) demanded the abolition of the regulation, but the federal government did not respond.

A similar § 20 Abs. 6 Satz 4 EStG (stocks) was submitted by the Federal Fiscal Court (BFH) to the Federal Constitutional Court (BVerfG) in 2020 due to a violation of Art. 3 Abs 1 GG. By then, it was clear that Sentence 5 was also unconstitutional.

The Financial Market Stabilization Acceleration Act (ZuFinG) aimed to repeal the above two sentences, but the Chancellor's Office removed it.

According to Art. 93 Abs. 1 Nr. 2 GG, each state government has the opportunity to submit an obviously unconstitutional law to the BVerfG. Why has the Bavarian State Government so far omitted to do so, thus exposing Bavarian taxpayers to the law?

Answer (translated)

I seek your understanding as I can only respond here as a representative, not a member of the state government.

My research has shown:

The restriction on income tax deductibility of losses from futures trading was initially viewed critically by Bavaria. Ultimately, the regulation was supported in a political compromise to prevent more extensive limitations. Further restrictions on losses from option expiration and worthless capital investments were thus avoided.

The assessment that the limitation on loss offsetting is "undeniably" or "obviously" unconstitutional due to a violation of Art. 3 para. 1 of the Basic Law (GG) is not shared. The Bavarian State Government would not have agreed to the legislative process in the Federal Council in this case. While there are numerous critical voices in the literature, there are also commentary opinions that consider the norm constitutionally compliant (e.g., Ratschow in Brandis/Heuermann / Income Tax Act § 20 / 166th Ed. February 2023).

Dear Mr. P., contrary to your opinion, it is still undetermined whether the provision of § 20 para. 6 sentence 4 Income Tax Act, which regulates the offsetting of losses from the sale of shares, is actually unconstitutional.

For the state government, initiating an abstract norm control procedure is only considered for politically significant topics or socially significant issues.

For individual taxation, affected citizens themselves have the option to initiate procedures to examine the constitutionality of a law.

Regarding the constitutionality of § 20 para. 6 sentence 5 EstG, a model suit was filed on May 24, 2023, at the Finance Court of Baden-Württemberg under file number 10 K 1091/23.

If the Finance Court considers this provision unconstitutional, the procedure will be suspended to obtain decisions from the Federal Constitutional Court.

That's the information provided.

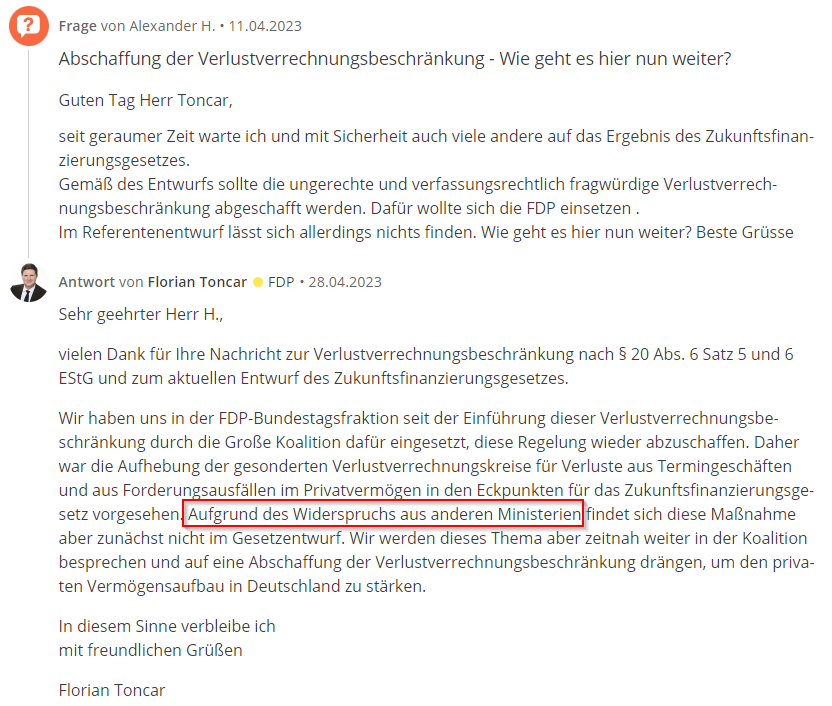

FDP - Florian Toncar

Bundestag Profile | abgeordnetenwatch.de Profile | Wikipedia (de) | Wikipedia (en)

Not a "perpetrator" per-se but being the FDP the tenant in the Ministry of Finance after the new general election, it is difficult to assimilate for taxpayers, that the Bindingsteuer still lives and the FDP has bowed to and before the SDP.

This after Florian Toncar was the outspoken opponent of the Bindingsteuer and was even interviewed in the same "Der Zertifikateberater" issue as Lothar Binding, expressing directly his doubts about the constitutionality already back then.

Granted, Herr Toncar has answered all questions from taxpayers stating that the topic has not been forgotten, and will be further discussed within the coalition.

And a public attempt was made to undo the damage, with the first paper for a "Future Financing Act" .

But still, promises are just promises and nothing more unless they are fulfilled. It is a lot more comfortable to let a proposal be vetoed and await the judicial path and a decision of the Federal Constitutional Court than to stand up and finish off a clear unconstitutional law, which was identified as such by the Federal Council (Bundesrat) from day one.

Let us at least recall how the "Future Finance Act" was botched by some other ministry.

The Bindingsteuer will live on because ...

Original

"Aufgrund des Widerspruchs aus anderen Ministerien findet sich diese Maßnahme aber zunächst nicht im Gesetzentwurf."

Translated

"However, due to opposition from other ministries, this measure is not initially included in the draft law."

Link: Toncar - abgeordnetenwatch.de - Veto from other ministries

A screenshot for future generations.

Lothar Binding - The Long Play Edition

Herr Binding is, allegedly, the intellectual author, the formal way of saying that he is the father of the beast.

Yes, the law was voted in parliament, so it has many parents. But before that it was crafted in the Finance Committee, where the real ones were.

The Finance Committee Smoking Gun

And the working document had only three people working on it and only two of them were from parties that voted for it, whilst the third did not (Green party). That means there are actually two choices left as seen in the Finance Committee - Recommendation and Resolution Report - 19/15876

- Sebastian Brehm (CDU/CSU)

- Lothar Binding (SPD)

In that same document, the situation clarifies itself. The last-minute change which introduced the Bindingsteuer was a joint amendment proposal from both parties (which formed the government coalition)

Page 2 - Section D

Original

Zu Änderungsantrag Nr. 11 der Koalitionsfraktionen der CDU/CSU und SPD (Beschränkung der Verlustverrechnung bei Einkünften aus Termingeschäften und aus dem Ausfall von Kapitalanlagen im Privatvermögen)

Translation

To amendment proposal No. 11 of the coalition factions of CDU/CSU and SPD (Limitation of loss offsetting for income from futures trading and from the failure of capital investments in private assets)

Although the jury is still undecided, page 38 first says that the CDU/CSU complains about how difficult was for the party to concede and reach a compromise with the SDP.

Page 38 - The CDU/CSU complains

Original

Schließlich machte die Fraktion der CDU/CSU darauf aufmerksam, dass der Änderungsantrag Nr. 11 der Koalitionsfraktionen, der in § 20 Absatz 6 EStG eine Beschränkung der Verlustverrechnung bei Einkünften aus Termingeschäften und aus dem Ausfall von Kapitalanlagen im Privatvermögen vorsehe, ein Kompromiss zwischen den Koalitionsfraktionen gewesen sei. Der Kompromiss sei aus Sicht der Fraktion der CDU/CSU schwierig gewesen. Es handle sich um ein schwieriges und komplexes Thema, da beispielsweise unterschiedliche Verluste

Translation

Finally, the CDU/CSU faction pointed out that amendment No. 11 of the coalition factions, which envisages a limitation on the offsetting of losses in income from futures trading and from the failure of capital investments in private assets in § 20 (6) of the Income Tax Act, had been a compromise between the coalition factions. The compromise had been difficult from the perspective of the CDU/CSU faction. It was a difficult and complex issue, as, for example, different types of losses

And the SPD confirms the CDU/CSU has complained, but finally bowed before its master.

Page 38 - Victory for the SPD

Original

Die Fraktion der SPD bestätigte, dass dieser Kompromiss auch von Seiten der Fraktion der SPD als schwierig empfunden werde

Translation

The SPD faction confirmed that this compromise was also perceived as difficult by the SPD faction.

And it is a clear win for the SPD and Lothar Binding, as the most probable intellectual author and father of the Bindingsteuer.

Recall that ...

The Bindingsteuer which deals with private individuals trading with derivatives (Futures, Options, CFDs) was introduced using a backdoor.

It is part of the law changes introduced with

Original

Entwurf eines Gesetzes zur Einführung einer Pflicht zur Mitteilung grenzüberschreitender Steuergestaltungen

Translation

Draf of the law for introducing an obligation to disclose cross-border tax arrangements

Yes, you have read right, buried within a law for cross-border tax control, the Bindingsteuer was born. See History for more details.

Public Defense and Mocking

Were the Finance Committee Smoking Gun the only evidence at hand, it would have been difficult for the mortal taxpayers, i.e.: all taxpayers, to have made a connection and the name Bindingsteuer may never have been born.

But Herr Binding was adamant and in several occasions made a passionate public defense of the benefits of the Bindingsteuer. Everybody knows that being expropriated is nothing but full of benefits.

Note

For sure some savvy persons who followed the issue right from the beginning, may have tracked the Bundestag documentation and finally named the tax, without any public statements from Lothar Binding.

There are two different arenas in which Lothar Binding was a merciless defender of the Bindingsteuer and where he mocked taxpayers. Some people would say that was defamation, but because it was not directed a specific person, rather a group, there would be no legal injury to repair and hence "defamation" would not legally apply.

- March 2020 Issue of "Der Zertifikateberater" ("The Tax Advisor")

- abgeordnetenwatch.de - Lothar Binding - Profile

Let us go for them.

Binding in "Der Zertifikateberater"

First, let us recall from the history ) that the Ministry of Finance, ironically, excluded Certificates and Warrants from the effects of the Bindingsteuer.

Ironically, because it was in the "The Certificate Advisor" where the first merciless defense was done.

Link: Der Zertifikateberater - March 2020 - Binding

Last but not least, what he said at the end of the interview.

Translated for dummies: stop trading or you will suffer the consequences

Nein. Die Idee ist es, solche risikobehafteten Geschäfte im privaten Bereich nicht steuerlich zu fördern. Wenn private Anleger sich in Zukunft zweimal überlegen, ob sie an der Terminbörse riskante Wetten eingehen wollen, und wenn wir dazu beigetragen haben, dass sie davon Abstand nehmen, dann haben wir unser Ziel erreicht.

Translation

No. The idea is not to promote such risky transactions in the private sector from a tax perspective. If private investors in the future think twice about engaging in risky bets on the futures market, and if we contribute for them to refrain from doing so, then we have achieved our goal.

The goal is clear, force people to think twice before trading and that the stop trading. And the goal is achieved with the

- Infinite () Tax Rate

- Taxes on Losses

- Eternally Growing Non-Recoverable Losses

What in plain English amounts to: Expropriation.

Notice that Herr Binding says "wir" ("we"). That is a constant during the interview and because we have seen from the Bundestag documentation that the SPD was responsible, it is clear who is "we": the SPD, with Herr Binding being the SPD commanding officer ("Obmann") in the Finance Committee.

Another gotcha moment.

Taxes on Losses

Original Question and Answer

Selbst wenn es so wäre, dass nur wenige Anleger Derivate in dieser Form einsetzen, würden Sie diese hart treffen. Denn durch die Begrenzung der Abzugsfähigkeit auf 10.000 Euro im Jahr ist es jetzt tatsächlich möglich, dass ein Anleger Steuern zahlen muss, obwohl er wirtschaftlich Verluste erzielt hat. Ist das Steuergerechtigkeit?

Steuergerechtigkeit ist so eine Sache. Anleger profitieren mit privaten Kapitaleinkünften vom günstigen Abgeltungssteuersatz. Es ist ein enormes Entgegenkommen des Staates, dass Gewinne aus Wertpapiergeschäften im Rahmen der Abgeltungsteuer vergleichsweise niedrig besteuert werden. Um Steuergerechtigkeit herzustellen, müssen wir dies erstmal überdenken.

Translation

Even if it were the case that only a few investors use derivatives in this way, it would hit them hard. Because by limiting the deductibility to 10,000 euros per year, it is now possible for an investor to actually pay taxes even though they have incurred economic losses. Is that tax fairness?

Tax fairness is a tricky issue. Investors benefit from the favorable flat withholding tax rate on private capital income. It is a significant concession by the state that gains from securities transactions are comparatively lightly taxed under the flat-rate withholding tax. To achieve tax fairness, we need to rethink this first.

Wow! Notice that he has acknowledged that people will be taxed on losses, but he hides behind the "Tax fairness is a tricky issue" and long series of bla, bla, blas.

After this interview, anyone related to the trading world had already assigned the fatherhood and intellectual authorship to Lothar Binding.

The interview is full of gotchas and a repetition of the same flawed, fake and bullshit arguments that were used to defend the enacting of the law.

Gotcha: Other taxpayers pay for trading losses

Original

Bisher ist es so, dass einige Trader, die sich auf den Handel mit Derivaten spezialisiert haben, sehr hohe Risiken eingehen, um überproportional hohe Gewinne zu erzielen. Gehen die Wetten nicht auf, bürden diese Anleger den Steuerzahlern ihre Verluste auf.

Translation

Currently, some traders who specialize in derivatives trading take very high risks to achieve disproportionately high profits. If the bets fail, these investors shift their losses onto taxpayers.

Fake! Alternative facts! If a trader loses money, it is first compensated against the winnings and if excess losses remain, they are carried over to the following years. This is NEVER shifted onto other taxpayers.

If Herr Binding is aware of how the traders can pass the losses to other taxpayers and get money from the state, he should please share it with the world.

And the "mocking" (defamation for some people) for some starts already in the interview.

Mocking the traders

Original

Wer privat mit Derivaten zocken will, darf das gerne tun, muss dann aber oberhalb der Verlustabzugsbeschränkung auch das Risiko alleine tragen.

Translation

Anyone who wants to gamble privately with derivatives is welcome to do so, but above the loss deduction limitation, they must bear the risk alone.

Yes, there is no mistake here: "zocken" is German for "to gamble". It is clear that for Herr Binding traders are simply gamblers.

Binding on abgeordnetenwatch.de

Here was he even more adamant and vocal in his "abgeorndetenwatch.de - profile "

His answers to the questions concentrate on the same flawed arguments:

- Gamblers

- Risky Bets

- Other taxpayers assume losses

- Protecting private investors

A collection of his answers with some of the most shocking statements.

In line with the objective net principle?!?!

Link: Frage an Lothar Binding von Thorsten K. bezüglich Finanzen

Original

Auch hier ist ein unterjährig begrenzter Verlustabzug innerhalb der gleichen Einkunftsart möglich und auch hier gilt, dass ein Verlust sich steuerlich nicht schon im Veranlagungsjahr seiner Entstehung auswirken muss. Daher geht die neue Regelung aus § 20 Abs. 6 Satz 5 EStG konform mit dem objektiven Nettoprinzip und entspricht dem Leistungsfähigkeitsprinzip.

Translation

Here too, a loss deduction within the same category of income is possible within the year, and here too, a loss does not necessarily have to affect taxes in the assessment year of its occurrence. Therefore, the new regulation in § 20 (6) sentence 5 of the Income Tax Act is in line with the objective net principle and corresponds to the ability-to-pay principle.

One can only be amazed. He states that the offsetting of losses is limited and a few words later he says that everything is in line with the objective "net principle", which means only the "net" is taxed.

As we have seen with "Real Cases" and "Math (for Children)" the net result of the trading year is not taxed. A fake virtual net profit is limited. Even the Bundesrat immediately recognized it and realized this would "indefinitely" tax winnings and avoid offsetting losses.

(/sarcasm on) Everything of course "in line" with the objective net principle (/sarcasm off)

Expropriate you to protect you

Link: Frage an Lothar Binding von Roman L. bezüglich Öffentliche Finanzen, Steuern und Abgaben

Original

Wenn Ihre Altersvorsorge tatsächlich davon abhängt, dass Sie privat am Kapitalmarkt spekulieren müssen, dann ist es vielleicht tatsächlich besser, ich schütze Sie vor sich selbst

Translation

If your retirement actually depends on your need to speculate privately in the capital market, then perhaps it is indeed better for me to protect you from yourself.

Socialism knows always better what is good for the people. And Herr Binding now talking in 1st person, as father and intellectual author, has introduced a law which can expropriate people to protect them from themselves.

Furthermore, the trader may be willing to protect a portfolio of shares for the retirement age, using Options as the insurance. But the trader can no longer use them thanks to the Bindingsteuer. As seen in the next entry.

Reading is believing.

Investors do not only uses derivatives for protection ...

Link: Frage an Lothar Binding von Brigitte J. bezüglich Öffentliche Finanzen, Steuern und Abgaben

Original

Denn Termingeschäfte werden von privaten Anlegern nicht nur zur Absicherung von Fremdwährungsrisiken, Marktrisiken oder zur Absicherung von Zins-, Preis- oder Kursniveaus getätigt, wie es bei Unternehmen aus realwirtschaftlichen Motiven die Regel ist, sondern maßgeblich zum "Zocken"

Translation

Because private investors engage in futures trading not only to hedge foreign exchange risks, market risks, or to hedge interest, price, or price levels, as is the norm for companies for real economic reasons, but mainly for "gambling".

His obsession with "Gambling" is again visible (in each answer actually), but the incredible thing is that he acknowledges private investors use derivatives to protect things against risks and he does not care, because his crusade is against his belief in "gambling".

What reminds of past prohibitions around the world, like alcohol prohibition and many others.

And finally.

Hey, a tax was named after me

Link: Frage an Lothar Binding von Andreas R. bezüglich Finanzen

Original

"Die Bindingsteuer wird 2021 zum Einsatz kommen". Bislang war mir noch gar nicht bekannt, dass eine Steuer nach mir benannt wurde.

Translation

"The Bindingsteuer will come into effect in 2021." So far, I was not even aware that a tax was named after me.

After some research, he found out that the tax was named after him. Name is confirmed.

Conclusion

It should be clear why taxpayers believe that Lothar Binding is the intellectual author and father of the Bindingsteuer. He even found out himself already in 2020.