The Law (for Dummies)

The banana-republic-like law, formally referred as "§ 20 Abs. 6 Satz 5 EStG" ("Income Tax Law - Section 20, Paragraph 6, Sentence 5") is aimed at capital gains made trading with derivatives.

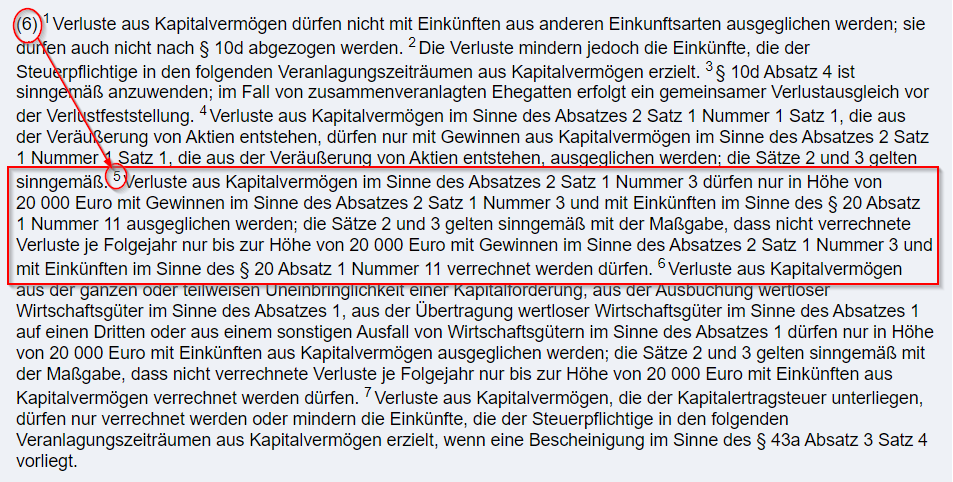

Given how much is achieved with such a short content, one has to admire the evil beauty of the modifications made by the SPD team. See with your own eyes.

Reference: Justice Minister - Law Online

Translation for mere mortals

-

When trading with derivatives a maximum of

20,000EUR in losses can be used to calculate the net profit, i.e. taxable amount, and only against derivatives. -

The non-compensated losses can be offset the following years, but up to a maximum of

20,000EUR each year.

Some quick and dirty numbers to better grasp it all. This is what commonsense people and laws abide by:

Winnings: 100,000 EUR

Losses: 100,000 EUR

Net Profit: 100,000 - 100,000 = 0 EUR

But because the Bindingsteuer limits the maximum losses to offset to 20,000 EUR.

Binding-Net-Profit: 100.000 - 20,000 = 80,000 EUR

And now taxes are paid on a fake virtual profit of 80,000 EUR. The fake virtual net

profit has been magically created out of thin air.

Hence the new name, in harmony with the tax name for the fake virtual net profit: "Binding-Net-Profit". Some other terms will also be prefixed with "Binding-", when they are changed by the law or are tightly coupled to it.

THE EFFECT - Private Bankruptcy

World First: A Law which Can Drive People into Bankruptcy

And this is because, as quickly seen above and in detail below, the Bindingsteuer will not tax real profit, but a fake virtual net profit, the Binding-Net-Profit, which will therefore tax directly the taxpayer's private assets.

And there is no limit as to how much, hence the risk of private bankruptcy.

See the real case of The Infinity-Millennium Trader Max

Let us carry on and see how this is possible.

Effect #1 - Unlimited Taxing of Everything

An Unlimited Tax Rate

Yes: Unlimited.

As soon as losses exceed 20,000 EUR, winnings will no longer be compensated and this

means that the tax rate starts escalating and the limit is Infinity

.

Taxes on Losses

If the derivatives trader had a losing year, only 20,000 EUR of the losses will be

considered, which means that any winnings exceeding 20,000 EUR will be taxed,

leading therefore to taxing losses.

Lothar Binding acknowledged the taxes on losses concept in an interview in "Der Zertifikateberater" ("The Certificate Advisor") and he did not care. Lothar Binding - Der Zertifikateberater

Effect #2 - Expropriation

Technically one would say: "Taxing of Private Assets". Because it is simply a technicality, is it not?

Losing Trading Year

A net loss was made. The loss-offsetting limit will create a positive virtual Binding-Net-Profit out of thin air and with it a real tax amount to pay.

Which means the due tax amount will be taken straight out of the pocket of the taxpayer.

Winning Trading Year

Even in this case, the net profit will be magically made gigantic by the

loss-offsetting limit. See the example above in which a 0 EUR net profit was

transformed into a virtual Binding-Net-Profit of 80,000 EUR.

Soon enough due taxes will exceed the real net profit and will take money straight out of the pocket of the taxpayer.

See: Math (for Children)

Se also any of the Real Cases

Effect #3 - Eternally Growing Unrecoverable Losses

Non compensated losses are left in a state of flux, which would be ideal to power the Delorean's Flux Capacitor, but the Binding-Losses are incombustible and therefore eternal.

The never ever compensating Binding-Losses

Any loss above 20,000 EUR, Binding-Losses, can be compensated the following

years, but only up to 20,000 EUR per year.

This creates an impossible conundrum, because to actually be able to offset the

carried-over Binding-Losses, one would need to trade losing less than 20,000 EUR

(before the real Net Profit/Loss is calculated)

Being this the real life and not the Binding-Verse, perfect trading does not exist and having real losses, compensated with winnings, is natural. And because of this the carried over losses from the previous year will not be really compensated.

See the real case of The Infinity-Millennium Trader Max

Effect #4 - Portfolio Insurance is Forbidden

Thou Shall Not Save Thy Portfolio

To protect a portfolio of shares against sudden downfalls, one would use Options. In most cases the downfall will not happen, and the money paid for the options will have been the insurance price.

But being cross-compensation forbidden by the Bindingsteuer, any price paid for the Options as insurance is gone, because it cannot be compensated with winnings from the portfolio of shares.

Lothar Binding acknowledged the new incarnation of the law forbids this in an interview in "Der Zertifikateberater" ("The Certificate Advisor") and he did not care. Lothar Binding - Der Zertifikateberater

Warning

It would seem that compensating losses with shares against winnings with derivatives would still be a valid option, but the sister tax, the Aktienbinding (another popular name), formally "§20 Abs. 6 Satz 4 EStG", ensures this is also not possible, because it forbids loss-offsetting in the other direction.

Aktienbinding is already in the hands of the Federal Constitutional Court awaiting a decision as the Federal Fiscal Court doubted its constitutionality in November 2020 and raised therefore a question to the highest court.

See: BFH - Decision 17.11.2020, Az. VIII R 11/18

It shall be noted that Aktienbinding is a lot less destructive than the Bindingsteuer and yet the Federal Fiscal Court cannot see how it can fit in the constitution.

Effect #5 - Derivatives Products Affected

This is not actually defined explicitly by the law, which only mentions "Termingeschäfte". For non-German speakers, "Termin" means "appointment", i.e.: the expiration date for Futures and Options.

But the Ministry of Finance defined the affected products in June 2021, with the law already 6 months in motion. Yes, to add to the insult, during 6 months nobody knew what was really within the scope of the law.

Yes, Olaf Scholz, the maximum responsible, was still Finance Minister and Lothar Binding was still the SPD Finance Speaker.

See the history for the document: "Bundesministerium für Finanzen - Schreiben Juni 2021"

Affected Derivatives

- Futures

- Options

- CFDs

Yes, CFDs have no expiration date (no "Termin") but are still considered a derivative by the Ministry of Finance, who removes the expiration date from the definition of derivative and declares that anything tracking another product is a derivative.

But the most incredible thing is what follows.

Non-affected Derivatives

- Certificates

- Warrants

Yes, derivatives issued by private banks are not affected.

This is an incredible twist, because the affected derivatives are negotiated in open exchanges under public scrutiny and where the price formation is the result of the pressure of the buying-selling sides.

As opposed to the privately issued derivatives, which work in black-box mode and where price formation is determined by the issuer.

With all that in mind, any reader is entitled to ask the question as to which powers and influence are granted to the bank lobbies, to have private black-box derivatives excluded from the consequences of the law.

Conclusion

The law has been translated to two clear and concise sentences and the perverse effects briefly explained:

- Private Bankruptcy

- Unlimited Tax Rate

- Taxes on Losses

- Eternally Growing Unrecoverable Losses

- Expropriation

- Portolio Insurance is Forbidden

- Only open-traded derivatives are affected, private black-box lobby-supported derivatives are not affected.

See the other sections for more information.