The Undoing

Undoing the perverse effects of the Bindingsteuer has three different routes.

Abstract

- Judicial

- Politics

- Do It Yourself (DIY - Actually, Working around it, with more or less overhead)

Because nothing can be expected from the current breed of politicians (see below) and the DIY approach is not a solution but a workaround with lots of overhead, let us start with that seems the only real way to have the problem solved: Judicial.

Judicial: The Court Path

This path is actually a closed one and starts with the Steuerbescheid (Tax Assessment) and has only one possible final station: the Bundesverfassungsgericht (Federal Constitutional Court).

No other instance can interpret or re-interpret the law.

What the Lower Instances Can Do

-

Finanzamt (Tax Office): Apply the law

After applying the law and after the formal complaint has been filed, the case can be put on hold under a number of different circumstances, for example: a case on the same topic is awaiting a decision in the Federal Fiscal Court (BFH), but the Tax Assessment (Steuerbescheid) will have been issued according to the valid text of the law. -

Finanzgericht (Finance Court)

Send a question about the constitutionality to either the Bundesfinanzhof of directly to the Bundesverfassungsgericht (or just wait, in case other case already did that) -

Bundesfinanzhof (Federal Fiscal Court)

Send a question about the constitutionality to the Bundesverfassungsgericht, i.e.: the Federal Constitutional Court (or just wait, in case other case already did that)

After which the highest instance is in play.

And the Bundesverfassungsgericht rules

The Federal Constitutional Court rules the Bindingsteuer unconstitutional.

Can it actually be any other way?

To be fair, it could be that we live in a universe in which expropriating people for engaging in an economic activity can be compatible with and fit within a constitutional text. Be ready if that is the case, because the Bindingsteuer, having paved the way, will be the least of your worries.

The first of the lower instances, the Finanzamt is not really part of the judicial path, because it is an administrative instance, but the taxpayer is obliged to comply with the formalism of formally filing a complaint to avoid forfeiting rights. And so it goes.

The Finanzamt Ping-Pong

sequenceDiagram

participant TP as Taxpayer

participant FA as Tax Office (Finanzamt)

TP -->> FA: File Taxes

FA -->> TP: Tax Assessment

Note over TP: Bindingsteuer!?!?

Note over TP: Infinite tax rate?!

TP -->> FA: Complaint!!!

Note over FA: Sorry, the SPD forced our hand.

FA -->> TP: Bindingsteuer it is: rejected.Note: Several communication rounds may be needed

Once things are over with the Tax Office, which can take up to 12 months, and within a month of the final decision made by the Tax Office, it is time for the lawsuit.

The "Closed" Judicial Path

flowchart TD

TP(Taxpayer) -- Lawsuit (within 1 month) --> FG[Finance Court]

FG --> BFH[Federal Fiscal Court]

FG --> BVERFG[Federal Constitutional Court]

BFH --> BVERFG

BVERFG --> U>Unconstitutional]Note: Simplified flow without potential appeals, costs and lawyers where needed.

Notice how the judicial path is categorized as "Closed". And it is, because the path has only 1 entry point and 1 exit point. All roads lead to Rome, sorry, to the Federal Constitutional Court, aka "Bundesverfassungsgericht".

Judicial: Actual Court Cases

Four cases are known.

1. Already at the Federal Fiscal Court (BFH)

FG Ref: Finance Court of Rhineland-Palatinate: 1-V-1674/23

Fully detailed in the section Real Cases .

The case does not have a sentence in the Finance Court, but rather a decision preventing

the expropriation of capital, i.e.: that the taxpayers were obliged to pay

59,860 EUR in taxes, for having posted a net profit of 23,342 EUR.

This needs some clarification, because the taxpayer has gotten a positive decision, albeit partial, and the court still wants to make a full decision on the whole.

And it is already at the Federal Fiscal Court station, because because the Tax Office (Finanzamt) has filed and appeal. Yes, you are reading right: a court says it has real doubts about the constitutionality and it is therefore stopping the expropriation of a taxpayer and the Tax Office (Finanzamt) has nothing better to do that file an appeal instead of waiting for the full decision. It seems like someone is really willing to expropriate.

1.1 The initial outcome of this case in the Bundesfinanzhof

BFH Reference: BFH VIII B 113/23 . A decision was issued on June 7th, 2024.

Stay therefore tuned for this decision, which may:

-

Resolve only the conundrum of the confiscation

-

Look at the entire case and issue a question of constitutionality and forward it to the Federal Constitutional Court

The latter would mean that the case would have been accelerated by the appeal filed by the Finanzamt.

Unfortunately the initial action has been to only resolve the conumdrum of the expropriation.

Being fair then, it may be the Finanzamt wants also to have a quick full decision on the issue of the constitutionality of the Bindingsteuer to stop applying the atrocity. Hats off in this case to the Finanzamt.

The other cases are stuck at the Finance Court (FG) level.

2. other cases

-

CFD-Verband

Finance Court Baden-Württemberg - Az: 10 K 1091/23 - CFD Association Lawsuit Info -

Finance Court epizentrum (username in the forum, actual FG has not been disclosed)

- Finance Court Munich

#2 and #3 are known from the wallstreet-online.de forum. The CFD Verband made its case public, after having been looking for a candidate.

All three cases are awaiting a final decision from the judge but seeing how the first case progressed to the Federal Fiscal Court (BFH), because the Tax Office (Finanzamt) appealed, it may well be that the other three cases will await, or have to await, a resolution of the Rhineland-Palatinate case.

But something else popped up at the end of February 2024.

Another case? Resolution at Finance Court level soon?

CMS law.tax.future talks about 5 known cases and a decision being expected soon.

Link: CMS - 5 cases - Decision soon

Dated: Feb 27th, 2024

If the other 4 cases are the ones quoted above, CMS would be in charge of a 5th case and this would be the one expecting a decision, given that the others have no news (or no good news with regards to timing)

Politics - No Hope

Quick Summary

-

The SPD vetoes initiatives and still mocks traders in public, calling them gamblers and stating that derivatives are "risky bets".

-

The FDP, who opposed the enacting of the law and is in control of the Ministry of Finance, has made proposals, but bows to the SPD Masters when the time to execute comes.

-

The CDU has turned itself around and from voting with the SPD to enact the law is now filing motions to kill it, but #1 (SPD) and #2 (FDP) reject them.

Really unpromising, so let us see the facts.

SPD - Michael Schrodi

Being the actual Finance Speaker of the SPD, seeing his thoughts and position about the Bindingsteuer will give a crystal clear diagnostic as to what to expect from the SPD.

On the other hand, Olaf Scholz, the Finance Minister (and Chancellor today) who signed it, has never made any public statements (it may well be he does not knows what he signed) and his wingman back then, Lothar Binding, retired and is no longer in Parliament and made no further public statements.

Starting with Michael Schrodi is therefore the way to go.

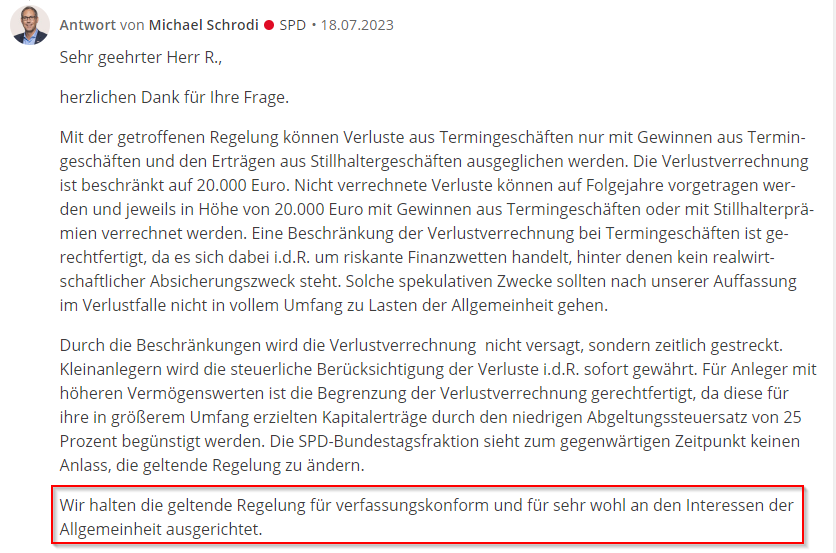

A question about the Bindingsteuer was addressed to him on abgeordnetenwatch.de on Jul 17th, 2023 and he actually answered one day later.

Summary: "Expropriation" is well aligned with the interests of the general public.

The term "Expropriation" has been added because he believes the law, which expropriates, to be well aligned with the interest of the general public.

Link: abgeordnetenwatch.de - Michael Schrodi 2023-07-18

Question (translated)

Loss Offsetting for Futures Transactions: Do the legal effects align so completely with the goals of the SPD that you see no need for changes?

Three reasons are cited for the limited loss offsetting for futures transactions:

1. Closing tax loopholes

2. Preventive deterrence

3. Avoidance of unilateral sharing of lossesHowever, it is not just about closing a tax loophole. The majority of those affected are likely to be tax-compliant private investors.

Deterrence does not primarily work preventively. Many private investors are unaware of the legal regulations. Only upon receiving tax assessments (and thus too late), are private investors deterred.

It is not only the unilateral but any sharing of loss transactions above €20K per year that has been excluded. The result is a unilateral sharing of profits.

I have incurred a significant loss. In addition, I am supposed to pay a similar amount in taxes. I perceive this as a punishment. Small government parties and the CDU see the need for changes. Only my party of heart does not...

Answer (translated)

With the current regulation, losses from futures transactions can only be offset against profits from futures transactions and income from option premium transactions. Loss offsetting is limited to €20,000. Uncompensated losses can be carried forward to subsequent years and offset in each year up to €20,000 against profits from futures transactions or option premiums. The limitation on loss offsetting in futures transactions is justified, as these transactions typically involve risky financial bets without a real economic hedging purpose. In our view, speculative purposes should not fully burden the general public in case of losses.

The restrictions do not deny loss offsetting but rather extend it over time. Small investors generally receive immediate tax consideration for their losses. For investors with higher assets, the limitation on loss offsetting is justified, as they benefit from the low flat tax rate of 25 percent on their more substantial capital gains. At present, the SPD parliamentary group sees no reason to change the existing regulation.

We consider the current regulation to be in line with the constitution and well-aligned with the interests of the general public.

Wow!

Let' quickly analyze the answer:

The Key Wrong Points

-

Expropriation is well-aligned with the interests of the general public. A classic in banana republics and dictatorships.

-

"risky financial bets", because who would use them to protect a portoflio as pointed out by the Bundesrat - Report

-

He has no problem in making false statements, like "speculative purposes, should not fully burden the general public in case of losses"

If he knows of a single tax case in which a private individual trading with derivatives burdened the general public, he shall please present it to the public. -

And hey, of course, mentions that losses are not lost, but can be carried over to the following years. As if they were recoverable:

-

Ask Max in his real case "The Infinity-Millennium Trader" ...

-

Ask the Bundesrat - Report ..., in which the non-recoverability and eternal growing is already stated.

-

But as it already happened in 2020, the motto still is:

Who the fuck is the Bundesrat?

A picture for the posterity.

FDP - Florian Toncar and the Financing Law of the Future

Florian Toncar, now Secretary of State, under Finance Minister Christian Lindner, since December 2021, was the voice against the introduction of the Bindingsteuer.

And the Ministry of Finance issued an initial proposal for a new act, titled: "Zukunftsfinanzierungsgesetz" (Future Financing Act) which can be found here: Key Points for a Future Financing Act

The Proposed End of the Bindingsteuer

Original

Damit wir auch eine wesentliche Vereinfachung im Abgeltungssteuerverfahren erreichen, wollen wir gleichzeitig die gesonderten Verlustverrechnungskreise für Verluste aus Termingeschäften und aus Forderungsausfällen im Privatvermögen aufheben.

Translation

In order to achieve a significant simplification in the flat-rate withholding tax procedure, we also want to eliminate the separate loss offsetting circles for losses from futures trading and from bad debt in private assets.

Some commonsense seemed to on the table, at last. But it only "seemed" so. Behind the curtains something happened and the first draft of the act came out (see: Future Financing Act 1st Draft ) with any reference to the removal of the Bindingsteuer gone with the wind.

And the death of the Bindingsteuer was no more

There was at least some light as to why. Florian Toncar said:

Original

"Aufgrund des Widerspruchs aus anderen Ministerien findet sich diese Maßnahme aber zunächst nicht im Gesetzentwurf."

Translated

"However, due to opposition from other ministries, this measure is not initially included in the draft law."

Link: Toncar - abgeordnetenwatch.de - Other ministries

Wow!

Everybody is entitled to believe that the "opposition" (veto, in fact) came from the SPD, seeing the public position defended by Michael Schrodi, and being Olaf Scholz the chancellor and previously the Finance Minister who signed off the legalization of expropriation in the form of the Bindingsteuer.

And the FDP ended up bowing before the SDP

The final form of the law did not bring back hope for Germany.

CDU/CSU - Fritz Güntzler

Incredible but true. The same CDU/CSU that voted for the enacting of the Bindingsteuer in exchange of some electromobility votes, requested now its removal.

Removal of the Bindingsteuer

Link: CDU/CSU Bindingsteuer Removal Request

Page 6 with regards to "§ 20 Abs. 6 Satz 5 EStG"

Original

b) Absatz 6 Satz 4 bis 6 werden gestrichen.

Translation

b) Sentences 4 to 6 of paragraph 6 will be deleted.

And in an incredible twist of fate ...

Even the FDP voted against

Yes, the FDP bowed before the SDP, this time in public.

Politics: The Conclusion

As seen above not much can be expected from the politics.

Abstract

-

The SDP positions itself in public against it, considers expropriation fantastic for society and vetoes the initiatives of other parties.

-

The FDP ... there is not much to say about the FDP and its delivery capacity. The trend in the polls (under 5%, out of parliament) say it all.

-

The CDU/CSU ... before something can be said, the CDU/CSU should make a public statement asking the German people for forgiveness for having supported the enacting of the Bindingsteuer.

Do-It-Yourself - DIY - Work around it!

DIY #1 - Self Imposed Trading Prohibition

This is actually the goal that Lothar Binding sought. No, this is not just the wish that it was so, he said it. In a interview in 2020 in "Der Zertifikateberater" ("The Certificate Advisor"), amongst many other blunt statements ...

The goal: A Trading Prohibition

Link: Lothar Binding Interview - Der Zertifikateberater

Original

"Wenn private Anleger von riskanten Wetten Abstand nehmen, haben wir unser Ziel erreicht"

Translation

"When private investors refrain from risky bets, we have achieved our goal."

Crystal Clear!

Translated into a language for dummies

Legalizing the infinite tax rate, taxes on losses and with all of it, expropriation, is directed at inflicting such a damage and pain, that the victims will refrain from trading and those seeing the victims will also refrain from trading.

Remember, all this comes from the "social" party ("Sozialdemokratische ...")

Lothar Binding wanted to also protect investors from themselves by imposing this. See Binding on abgeordnetenwatch.de

DIY #2 - Trade Through a Company - A Trading GmbH

Yes, this works but

Pros & Cons

Pros

- Not affected by the Infinite Tax Rate or Taxes on Losses

- No effective prohibition of recovering the losses from a losing year

- No tax-induced bankruptcy

Cons

- Double the capital gains

25%tax rate to50% - Any Binding-Losses made before incorporating the company, cannot be compensated

- Overhead

Let us see the numbers quickly.

The Trading GmbH Case

The tax rates to consider are:

33%- Corporate Tax Rate25%- Personal Capital Gains Tax Rate

Net Trading Profit: 100,000 EUR

Corporate Tax (33%): 100,000 * 33% = 33,000 EUR

Net Profit After Taxes: 100,000 - 33,000 = 67,000 EUR

Capital Gain Tax (25%): 67,000 * 25% = 16,750 EUR

Net Profit After Taxes: 67,000 - 16,750 = 50,250 EUR

Total paid in taxes: 33,000 + 16.750 = 49.750 EUR

Effective Tax Rate: Total_Taxes / Net_Profit

Effective Tax Rate: 49,750 / 100,000 = 49.75%

As simple as that. Add the management fee to the calculation of the 49.75% tax rate and

the effective tax rate will go slightly over 50%, i.e.: doubling the personal tax rate

of 25%.

The associated management effort cannot be quantified in terms of tax rate, but it has to be taken into account, but the scheme works, after effectively doubling the tax rate.

DIY #3 - Move Abroad

Option which does also work but which involves having no ties binding the emigrant to Germany, like for example children attending school.

No, A Tax Paradise is not needed

Although the trader could move to the Virgin Islands, the following list of countries/territories are easier to go to and need no visa at all, just a plane ticket away or even a couple of hours in the car.

- Spain - Canary Islands

- Spain - Balearic Islands (Mallorca the 17th German Bundesland)

- Spain - Mainland (with lots of mediterranean coastal areas, some with ski resorts nearby)

- Italy - Lake Garda, South Tyrol and many other places

- Greece

- Portugal

- Malta

- Cyprus

- France

- Austria

- Croatia

- ... add your preferred EU destination to the list

Yes, move to the Canary Islands or to the 17th Bundesland (Federal State), Mallorca, and enjoy a life of trading on the beach.

Conclusion

Summary - Options to Undo/Work around the Bindingsteuer

-

Nothing to expect from politics, thanks to the "social" SPD supporting expropriation and knowing that the goal was to impose a prohibition.

-

The judicial path can be long, really long.

-

Stop trading and fulfill the dreams of the SPD

-

Use a GmbH, but doubling the capital gains tax rate:

25% => 50% -

Move abroad if you can and enjoy beaches, good food and fair treatment from the law.